If you’re an owner-operator or fleet manager, you’re not imagining things—freight rates in 2025 are still painfully low. Despite high fuel and insurance costs, average spot market rates have dropped below operating expenses.

The Freight Rate Freefall: What’s Going On?

The freight market is broken. Most loads pay far below operating costs. Owner-operators are running at a loss, while mega carriers survive on high volumes.

“I hauled a reefer load from Texas to Georgia for $1.65 a mile. It barely covered my diesel cost per mile.”

The Heartbeat of the Trucking Economy

Freight rates serve as a vital indicator for the economy. When they’re flatlining, it’s a sign of bigger problems.

- Consumer spending is sluggish

- Manufacturing orders are down

- Retail inventory is stagnant

A Brief Look Back: The Pandemic Freight Boom

In 2020-21, rates hit record highs. Trucks were in demand, and capacity was tight. But that surge led to an influx of new carriers and trucks. Now, we’re seeing the crash.

- Thousands of new authorities flooded the market

- Equipment orders spiked

- Now: overcapacity and low demand

Too Many Trucks, Not Enough Loads

With so many trucks chasing fewer loads, the math doesn’t add up. This is the core issue of the trucking recession.

- Capacity oversupply

- Shippers have more negotiating power

- Load boards are saturated

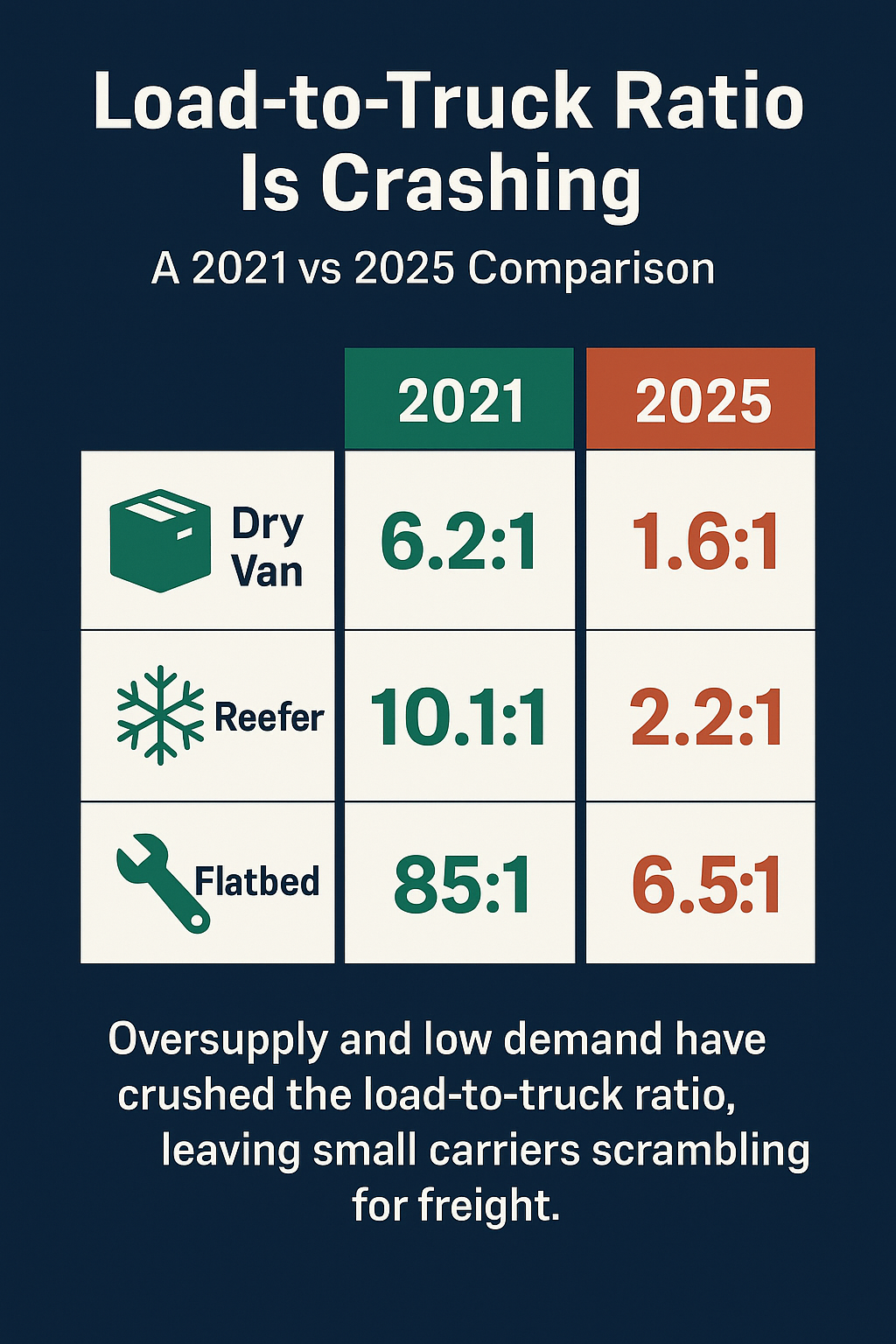

The Load-to-Truck Ratio Is Crashing

The load-to-truck ratio is crashing across all equipment types, with dramatic drops since the 2021 freight boom.

| Equipment Type | Peak Load-to-Truck (2021) | Current (2025) |

| Dry Van | 6.2:1 | 1.6:1 |

| Reefer | 10.1:1 | 2.2:1 |

| Flatbed | 85:1 | 6.5:1 |

Spot Market Blues: The Collapse That Hurts the Most

The spot market is in shambles. Small fleets and new authorities rely on spot loads, and those rates have crashed.

- The majority of lanes pay under $2.00/mile

- Fuel surcharges are inconsistent

- Brokers continue to push prices down

Mega Carriers vs. Owner-Operators

Mega carriers have leverage. They’ve got contracts, dedicated lanes, and volume discounts. Independent drivers? Not so much.

- Mega fleets undercutting independents

- Lower operational costs

- Load access priority

The Rise of Digital Freight Platforms

Apps like Uber Freight and DAT have changed the game, offering easier access, but at the cost of increased competition and reduced rate transparency.

- Load boards are flooded with low-paying freight

- Rates often don’t reflect real costs

- Small carriers lose negotiation power

Shippers Calling the Shots

Shippers now have the upper hand. High capacity gives them options—and they’re choosing the cheapest ones.

- More tenders going to mega fleets

- Shorter contracts, flexible pricing

- Delays in payment and delivery penalties

Consumer Demand Is Slowing Down

People are spending less, especially on physical goods.

- Retail sales are flat

- E-commerce growth has plateaued

- Fuel and food costs eat into discretionary spending

Retailers Are Still Sitting on Inventory

Warehouses are full. Until they move this stock, there’s no reason to restock.

- Lower order volumes

- Less freight movement

- Fewer long-haul runs

Imports Are Drying Up at U.S. Ports

Shipping volumes at major ports like LA, Long Beach, and Savannah have dipped.

- Less container freight

- Fewer intermodal opportunities

- Impact on both coastal and inland freight

The Domino Effect of Rising Interest Rates

The Fed’s rate hikes have stalled growth in housing, manufacturing, and retail.

- New construction down

- Equipment purchases delayed

- Freight demand contracts

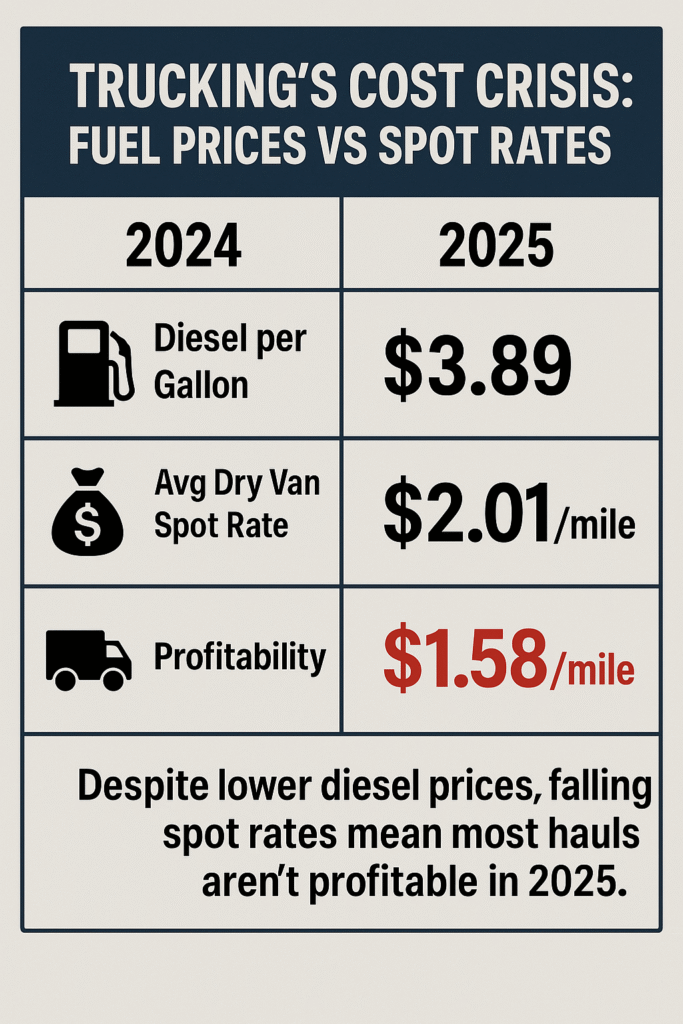

Fuel Prices Still High, But Freight Pay Is Falling

| Metric | 2024 Avg | 2025 Avg |

| Diesel per Gallon | $3.89 | $3.72 |

| Avg Spot Rate (Dry Van) | $2.01 | $1.58 |

Low freight rates in 2025 mean most hauls aren’t covering the diesel cost per mile.

Bankruptcies Are Surging in the Trucking Sector

FMCSA data shows over 9,000 carrier revocations this year alone.

- Small fleets shutting down

- New entrants exiting within 12 months

- Insurance and repairs are too costly

Where Did the Contract Freight Go?

Many shippers abandoned long-term contracts. They’re using spot rates or short-term bids instead.

- Contract stability is fading

- Rate volatility affects planning

- Owner-operators can’t rely on consistent income

Weather Disruptions Aren’t Creating Rate Spikes

Winter storms, hurricanes, and even floods used to increase rates. Not anymore.

- Too many trucks are waiting in every market

- Weather delays just cause downtime

- No rate advantage for risk

The Invisible Hand of Brokers

Some brokers are transparent. Others? Not so much.

- Rate info hidden

- Significant cuts taken before driver pay

- FMCSA transparency rules delayed again

Government Pressure and Regulatory Costs

2025 is a prep year for the EPA 2027 emissions compliance. That means upgrades, inspections, and costs.

- ELD enforcement increasing

- Safety audits ramping up

- Regulatory compliance is expensive

Driver Shortage Myth or Market Reality?

We don’t have a driver shortage—we have a driver turnover crisis.

- Drivers leaving due to low pay

- Burnout and long hours

- No incentives for new entrants

How Insurance Costs Are Breaking Small Fleets

Insurance is often the second-highest cost after fuel.

- Premiums up 12–15% YoY

- New carriers face sky-high rates

- Nuclear verdicts drive insurer caution

What Truckers Are Saying on the Road

“I used to run 3,000 miles a week. Now I park for two days just waiting for a load worth moving.”

“Freight rates are trash. We’re doing more work for less pay, plain and simple.”

Can the Market Rebalance in 2025?

It’s possible—but it won’t be fast. Here’s what needs to happen:

- Capacity needs to shrink significantly

- Demand must rise across core sectors

- FMCSA reforms to increase broker transparency

Staying Afloat in a Brutal Market

Smart survival strategies:

- Cut all non-essential expenses

- Focus on dedicated freight or direct shippers

- Monitor your cost per mile daily

- Join owner-operator forums for market updates

FAQs: Freight Rates and Trucking Industry Trends

Why are freight rates still low this year?

Rates remain low due to lingering overcapacity, high insurance costs, moderate consumer demand, and ongoing import slowdowns, as widely reported by FreightWaves.

When will freight rates rise again?

Modest improvements may come later this year if consumer demand improves and more carriers exit the market. Don’t expect a sharp rebound—more likely a slow recovery.

How much are truckers getting paid per mile now?

Dry van: ~$1.58/mile

Reefer: ~$1.87/mile

Flatbed: ~$1.75/mile

Is now a good time to enter the trucking industry?

It’s a tough time for newcomers. High startup costs and low rates make it a risky venture unless you have direct shipping relationships or a strong niche.

What should small fleets focus on now?

Controlling expenses, improving efficiency, diversifying freight types, and negotiating directly with shippers are essential strategies for staying competitive.

Conclusion: The Fight for Fair Freight

The freight market is in a bind, no doubt. Low rates, high costs, and fierce competition are pushing even experienced carriers to the brink. But this downturn isn’t permanent.

Truckers who survive today’s challenging market will be better positioned when rates finally rebound. Now’s the time to focus on what you can control: cut unnecessary expenses, maintain strong broker or shipper relationships, and be selective about the loads you haul.

It’s also a time to demand more transparency from brokers, platforms, and policymakers. Fair freight isn’t just about price. It’s about respecting the hard work that truckers put in every day.

Stay focused. Stay sharp. Better lanes are ahead. Read More